Caught in a Trap: A Liquidity Trap in the United States

By Leah Pieper '14

Intermediate Macroeconomics

Leah’s paper demonstrated not only an understanding of what happened in Japan in the 1990s, but was able to extend those results to discuss the economic problems currently facing the US. As a student in a sophomore level course, Leah far exceeded my expectations in economic analysis, but also in her ability to make difficult topics easier to understand. This was an exceptional piece of work.

-Brain Peterson

Despite being officially out of a recession for two years, the U.S. economy is not where the government—or the people—want it to be. Jobs are still scarce as many businesses continue to cut back. The continued stagnation of the economy has started many people wondering when and if the U.S. will ever get out of this crisis. Some economists are beginning to think that the U.S. has found itself in a situation known as a liquidity trap. Japan found itself in this situation in the 1990s when its economy stagnated after a recession. Signs that the situations are similar include the presence of zero-bound interest rates and the failure of open-market operations. Using evidence from Japan in the 1990s and current information on the state of the U.S. economy, this paper will compare the situations to determine if the U.S. is indeed in the same type of liquidity trap that Japan experienced. The actions of the Bank of Japan in response to the situation will also be examined, as well as the opinions of prominent economists to determine what actions the U.S. could take to get out of a liquidity trap.

Conditions of a Liquidity Trap There are two main characteristics to a liquidity trap: an extremely low interest rate and the ineffectiveness of open-market operations. Other symptoms include a recession and slow recovery (Weberpals, 1997). Wessel (2011) observes that interest rates must be low enough “that consumers, business, and investors don’t care if money is in cash or in interest-paying investments.” According to Weberpals, interest rates continue getting lower until they reach a critical rate, from which they cannot go any lower and money-demand will once again grow. When the interest rate is at the lower bound of zero, it is as low as it can go before holding cash becomes more profitable. For this reason, monetary policymakers cannot stimulate the economy in a liquidity trap (Abel, Bernanke & Croushore, 2011). Monetary policy, such as the open market operations usually used by the Federal Reserve, does not elicit as effective a response in this situation (Wessel, 2011; Krugman, 2010). The key sign that an economy is experiencing a liquidity trap is extremely low, zero-bound interest rates that hardly stimulate the economy at all.

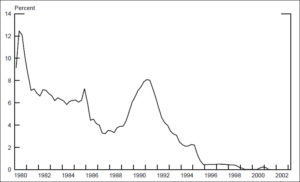

Japan’s Experience in a Liquidity Trap

Japan’s experience in the 1990s provides evidence of the occurrence of a liquidity trap. Japan’s overnight interest rate on uncollateralized loans (a measure similar to the Federal funds rate) was at zero in the 1990s. Economic growth had begun to slow in 1991, after the collapse of stock prices in 1989. This continued until the inflation rate hit zero in 1995 and then became negative (deflation) through 2005. The Bank of Japan responded by lowering the overnight interest rate from 8% in 1990 to below 0.5% in 1995 to stimulate the economy (Abel et al., 2011; Orphanides, 2003). However, this did not work, so the Bank of Japan reversed its policy. In 1998, the Bank of Japan decided not to attempt expansionary monetary policy because the Bank felt that the costs and benefits of doing so did not make it a viable option (Orphanides, 2003; Weberpals, 1997). This is clear evidence of the failure of open-market operations in Japan. The interest rate continued to move even closer to zero, averaging as low as 0.001% in 2004 (Abel et al., 2011; Murota & Ono, 2009). Figure 1 provides a history of the overnight interest rate in Japan. By the conditions established in the previous section, it is clear Japan was facing a liquidity trap in the 1990s.

Evidence of a Liquidity Trap in the United States

It is important to understand the U.S. financial crisis in order to understand how the possibility of a liquidity trap in the U.S. came about. Lowenstein (2010) provides a detailed analysis of the events leading up to the crisis in his book The End of Wall Street. The roots of the crisis go back to the early 2000s. The Fed lowered interest rates in the aftermath of the dot-com bubble and kept them low even after recovery; this stimulated economic growth by creating a lot of credit that increased borrowing. The policy worked, especially in the housing market. However, investors were not benefitting from the low interest rates, so they began to take on more risk to get higher yields. Lending to subprime borrowers became a popular way of doing this. By pooling mortgages and using financial instruments such as derivatives, financial institutions were able to make investing in the subprime mortgage market appear less risky. As the housing market began to weaken in 2005, the Fed significantly increased the interest rate because their most pressing concern at the time was inflation; the interest rate hit 5 % in 2006 and was kept high through 2007. When many subprime borrowers defaulted after the decline in the housing market, major financial institutions such as Fannie Mae, Freddie Mac, and Lehman Brothers began to experience serious liquidity problems. As the crisis deepened in 2008, banks and other lending institutions became increasingly wary of lending, investors were less willing to take on risk, and people were unwilling to borrow. It was clear that the U.S. economy had entered a recession.

Predictably, the Fed engaged in expansionary policy in response to the recession. In late 2007 and early 2008, the Fed lowered the interest rate several times. The economic situation then became so bad that the Fed decided to lower the interest rate close to zero in late 2008, despite fears that it could create the same speculative bubble that happened the last time those rates were low, at the beginning of the housing bubble (Murota & Ono, 2009). After allowing it to drop below 1% in late 2008, the federal funds rate stayed near or below 0.2 percent and is currently less than 0.1 percent (Board of Governors of the Federal Reserve System, 2011).

After the Fed began lowering interest rates in 2007, real GDP continued to fall through 2009. From 2007 to 2008, real GDP fell 0.3 percent and fell 3.5 percent from 2008 to 2009 (Bureau of Economic Analysis, 2011). The Fed is increasingly lowering interest rates closer and closer to zero, but this has not had much of an effect on the economy. Lowering the interest rate clearly has not stimulated growth much, at least not in the short run, indicating the ineffectiveness of open-market operations. The low interest rates, decreased effectiveness of open-market operations, and slow growth indicate that it is likely that the U.S. is beginning to experience a liquidity trap.

Japan’s Solutions

“viral” by Baily Miller

Japan tried numerous policies to remedy its situation. After concluding that lowering interest rates even further would not help in 1998, the Bank of Japan changed its mind. In February 1999, the Bank of Japan decided to keep interest rates as low as possible. Then in August 2000, it decided to tighten monetary policy because of expected improvement, but this did not happen. The Bank of Japan then expanded reserves in March 2001 (Orphanides, 2003). The Bank of Japan later tried to stimulate aggregate demand by expanding the monetary base between March 2001 and March 2006, but it had little effect since the money was absorbed as excess reserves, or money banks choose not to use for lending (Murota & Ono, 2009). In 2002 and 2003, Japan also tried “quantitative easing”—a method where the central bank prints more money and buys securities in the open market to reverse deflation. This method appears to have worked; the inflation rate increased during 2002 and 2003 and continued increasing, nearing zero in 2004 (Abel et al., 2011). Despite this one success, the overall Japanese economy continues to stagnate, as evidenced by continually elevated unemployment rates and renewed deflation (Murota & Ono, 2009). It may be still too early to tell the long-term effects of these policies, but as of now, the policies appear to have had little effect, and this makes the experience difficult to learn from.

Options for the United States

Based on Japan’s experience and the advice of prominent economists, there are plenty of options available to the U.S. One is to follow the classic Keynesian remedy—the government borrows and spends to stimulate demand and create jobs (Wessel, 2011). DeLong agrees with this idea for resolving a liquidity trap. He argues that “in this situation we need deficit spending. The government spends and borrows, creating more of the safe, cash-like assets that private investors want” (DeLong, 2011, p. 2). Another possible solution, suggests Svensson, is to devalue the currency to “jump-start the economy and escape deflation” (qtd. in Wessel, 2011, p. 2). Because the dollar is so important in the global financial system, this is not a likely solution for the United States.

A third way of escape is to create expectations of more inflation in the future without affecting the real interest rate. Kenneth Rogoff, a Harvard economist, supports this idea. If this solution were put in place, “incomes [would] rise with inflation, debts wouldn’t, and they’d be easier to pay off” (Wessel, 2011, p. 3). Bernanke agrees that something must be done about expectations. According to Bernanke, it is most important to take action “to affect the economy well before the public thinks that the central bank might be running out of ammunition. Once the public becomes convinced that monetary policy is powerless to help the economy, as may have been the case in Japan, affecting people’s expectations becomes much more difficult” (Abel et al., 2011, p. 555).

Krugman (2010) feels differently. He insists that the purchase of longer-term government securities or assets by central banks could help the situation. While this would be unconventional behavior for the Federal Reserve, Krugman believes that it would be better for the Fed to try this than to keep doing virtually nothing. Because interest rates are already so low, expanding further would not help the economy, so the Fed has not been doing much else. While the failure of open-market operations as a result of near-zero interest rates is a typical occurrence in a liquidity trap, Orphanides (2003) feels that monetary policy is not completely constrained. Orphanides contends that there is no limit on what a central bank can do—no matter how low the interest rate, monetary expansion is still possible. Because economics is not an exact science and the effects of certain policies may not be clear until years later, a central bank may “face substantial uncertainty about how and for how long it may need to pursue the expansionary monetary policy required to bring the economy out of a slump. Under these circumstances, the preferred mode of operations would be one that is as robust as possible to such uncertainties” (p. 20). Although the effects may not be immediately known, it is crucial to undertake further expansionary action. In other words, inaction is not an option.

Conclusion

There is evidence that the U.S. is in a liquidity trap. The prevalence of low interest rates and the ineffectiveness of open-market operations as indicated by continued stagnation provide evidence for a liquidity trap. The U.S. experience has been similar to the Japanese liquidity trap in the 1990s. If the U.S. can learn anything from Japan, it is that the future is grim. Despite repeated attempts to free the economy from the liquidity trap, Japan has stayed in a slump. The U.S. economy may also face long-term stagnation unless an effective solution can be implemented. Several possibilities have been suggested, but in the meantime, it may be best to brace for a slow recovery.

Figure 1. Overnight Interest Rate: Japan. From “Monetary Policy in Deflation: The Liquidity Trap in History and Practice,” by A. Orphanides, 2003, FEDS Working Paper No. 2004-01, p. 32.

Works Cited

Abel, A. B., Bernanke, B.S., & Croushore, D. (2011). Macroeconomics (7th ed.). Boston, MA: Addison-Wesley.

Board of Governors of the Federal Reserve System. (2011). Monthly federal funds (effective). In Selected interest rates. Retrieved from http://www.federalreserve.gove/releases/h15/data.htm

Bureau of Economic Analysis. (2011). Percent change from preceding period. In National income accounts: gross domestic product. Retrieved from http://www.bea.gov/national/index.htm#gdp

DeLong, B. (2011). The sorrow and the pity of another liquidity trap. Retrieved from http://www.bloomberg.com/news/print/2011-07-05/the-sorrow-and-the-pity-of-another-liquiditytrap-brad-delong.html

Krugman, P. (2010, March 17). How much of the world is in a liquidity trap? [Web long post].Retrieved from http://krugman.blogs.nytimes.com/2010/03/17/

Lowenstein, R. (2011). The End of Wall Street. New York, NY: Penguin.

Murota, R., & Ono, Y. (2009). Zero nominal interest rates, unemployment, excess reserves and deflation in a liquidity trap. Discussion Paper No. 748, The Institute of Social and Economic Research, Osaka University. Retrieved from http://ssrn.com/abstract=1433182

Orphanides, A. (2003). Monetary policy in deflation: The liquidity trap in history and practice. FEDS Working Paper No. 2004-01. Retrieved from http://ssrn.com/abstract=512962

Weberpals, Isabelle. (1997). The liquidity trap: Evidence from Japan. Bank of Canada Working Paper 97-4. Retrieved from http://ssrn.com/abstract=56139

Wessel, D. (2011, August). Finding a prescription for the U.S.’s money trap. The Wall Street Journal. Retrieved from http://online.wsj.com/article/SB10001424053111